In 1924, Ernie Dunn had a simple philosophy when founding our company: Get the best people you can get, give them interesting and challenging work, and let them share in the rewards. Our Employee Stock Ownership Plan (ESOP) is how that idea is lived out at JE Dunn today. The ESOP is a benefit that gives employees a stake in the company they help build, providing ownership over their work and contributing to JE Dunn’s collective success.

What is an ESOP?

An ESOP is a retirement benefit in which a company sets up a trust and provides employees with shares of company stock. Unlike a 401(k), contributions come entirely from the company.

As of 2026, there are over 6,400 ESOP companies in the U.S., covering more than 15 million employees, making it the most widespread form of employee ownership in the country.

Why ESOPs work

Studies by the National Center for Employee Ownership (NCEO) consistently find that employees at ESOP companies end up with significantly more retirement wealth than their peers elsewhere. One study found that ESOP participants have more than double the retirement assets of employees at comparable non-ESOP companies.

When your retirement savings are tied to the company you work for, your financial future rises and falls with its performance. That connection creates a level of alignment you don’t always get with traditional benefits — employees aren’t just earning a paycheck, they’re directly invested in the company’s success. Over time, that shared stake becomes part of the culture, shaping how people think, collaborate, and make decisions.

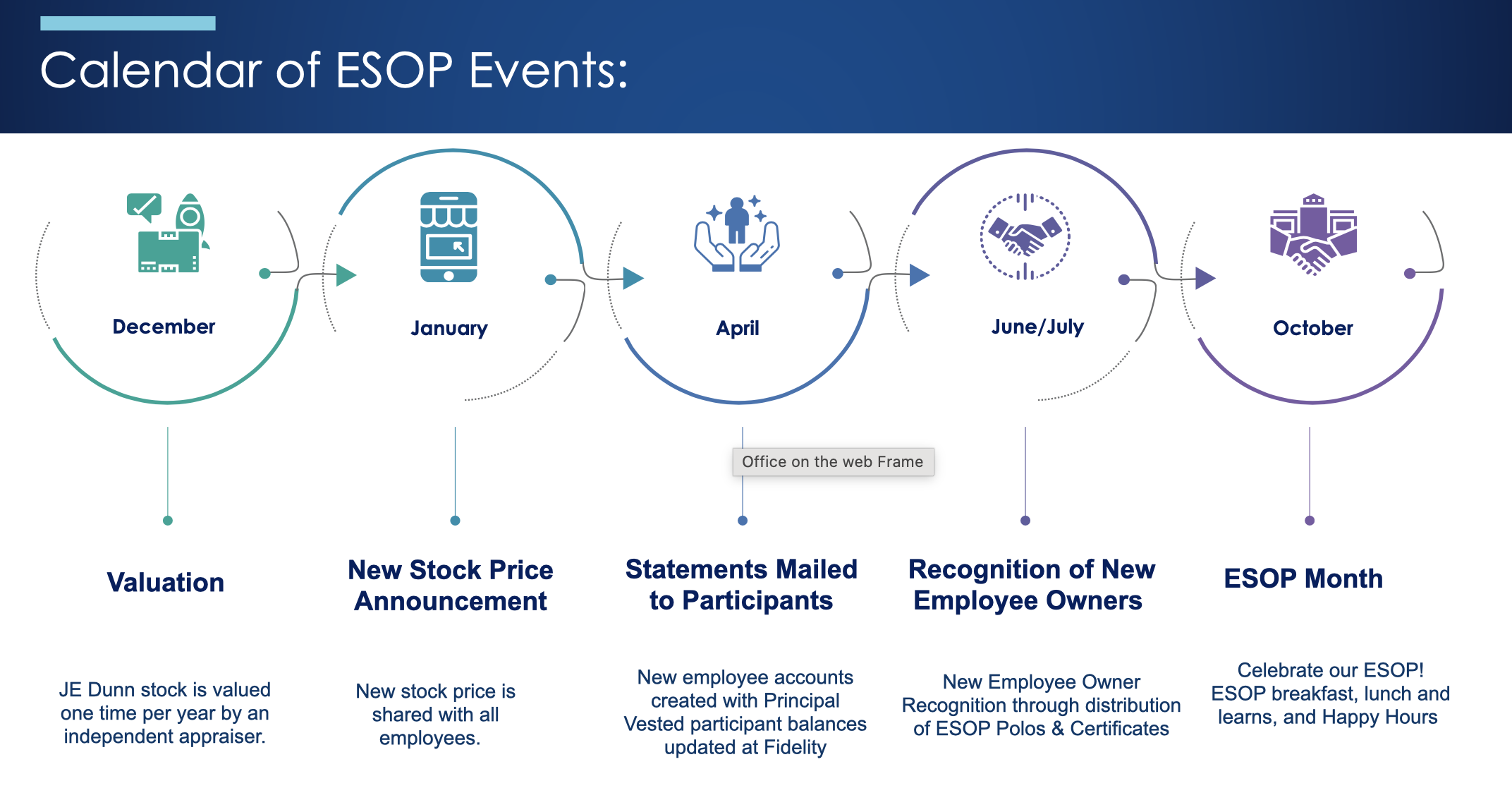

How JE Dunn’s ESOP works

Each December, an independent firm appraises JE Dunn to determine how much it’s worth, which determines the new share price. CEO Gordon Lansford announces the new price in January, and annual statements go out to employee owners in April.

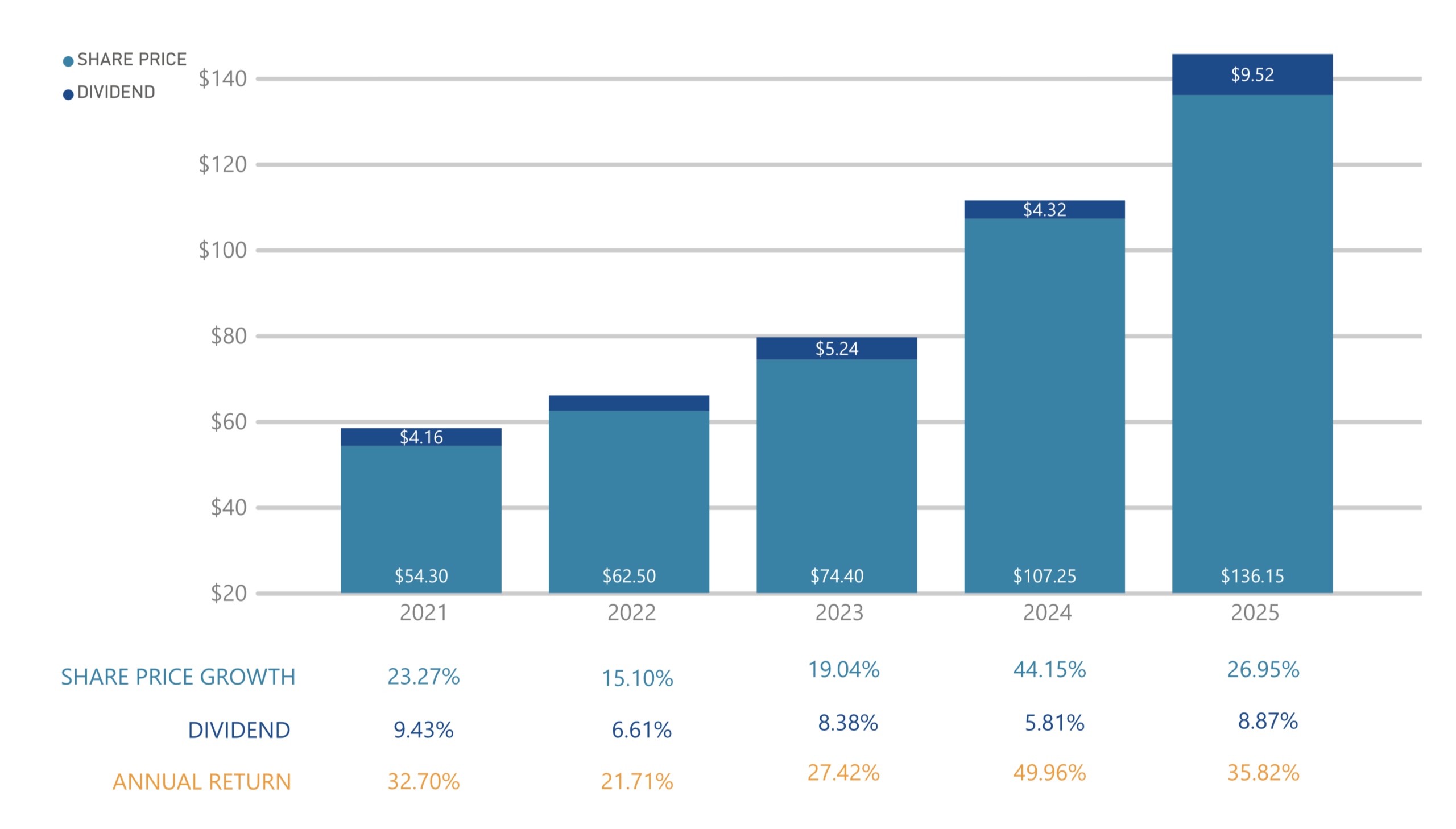

While past performance can’t guarantee future results, JE Dunn’s ESOP performance has increased every year since its creation in 2010.

While past performance can’t guarantee future results, JE Dunn’s ESOP performance has increased every year since its creation in 2010.

How to earn shares

How to earn shares

All full-time, non-union JE Dunn employees are eligible for the ESOP and earn shares two ways: through the 401(k) match and through discretionary profit sharing.

The 401(k) match starts as soon as you start contributing to the Dunn 401(k) Retirement plan, or as soon as 30 days of employment. JE Dunn matches 50% of the first 6% you contribute, for a maximum match of 3%. On $100,000 in eligible compensation, a 6% contribution earns a $3,000 JE Dunn match.

However, instead of depositing that match as cash into your 401(k), JE Dunn uses it to buy shares of the company, through our ESOP, in your name.

The second way that employees receive shares of JE Dunn stock is through the discretionary profit sharing. Profit sharing amounts can vary, since they are based on the performance of the company. Last year’s profit sharing reached 8%, the highest in company history. On that same example of $100,000 in compensation, $8,000 would be used to purchase shares of JE Dunn stock, in addition to the 401(k) match.

To ensure that you are maximizing this valuable benefit, all you have to do is contribute at least 6% to your 401(k).

Vesting

Vesting means ownership and determines how much of your ESOP balance you get to keep when you leave JE Dunn — based on hours worked, not on hire dates. Years in which you work at least 1,000 hours count towards vesting. After six eligible years of service, you’re fully vested, meaning you would receive your entire ESOP balance if/when you leave JE Dunn.

Employees aged 60 and older are automatically fully vested upon leaving, regardless of the years they’ve been credited in the plan.

Leaving or retiring

When you leave JE Dunn, your vested ESOP balance is yours and eligible for distribution in May of the following calendar year, valued at the updated share price. The ESOP is a Qualified Plan, which means that you can take cash (taxed as ordinary income) or roll your balance into a qualified retirement account like the Dunn 401(k) Retirement Plan or a personal IRA.

Leaving in January rather than December means your shares get valued at that new year’s appraisal, so payout is delayed, but you may benefit from another year of growth.

Resources

In addition to The ESOP Builder, the ESOP Calculator on Connect lets you model what your account could look like over time based on your compensation, current balance, and age. The numbers are hypothetical, but even conservative projections can give an idea of how your numbers may look upon retirement. Connect’s ESOP page also has key contacts, materials, and a video to help you understand this benefit.